Estimated reading time: 6 minutes

I was recently asked what merit raises should be based on – which is a great question!

Justification for a merit increase is important because of the financial investment the pay increase represents.

Merit increases can have a significant impact on an organization’s payroll cost over the span of perhaps decades that an employee works for an organization.

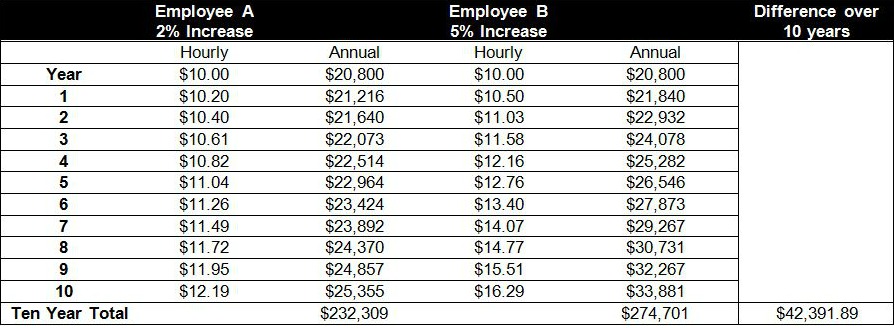

For example, let’s say you have two employees and each makes $10 per hour. Employee A receives a merit increase of 2%, and employee B receives a 5% pay increase.

The 2% increase is equivalent to $416 for the year and 5% equals $1040 for the year – more than double.

Multiply that by ten years and the employee who receives the higher increase will cost the organization much more over that ten-year period of time.

Now let’s say employee A gets 2% a year every year for ten years and employee B gets 5% every year for ten years and this is what it looks like:

As you can see employee B, who received the 5% increase over the course of ten years, cost the organization $42,392 more than employee A.

Now, do the math for the higher earners in your organization and the difference can be staggering.

This is why it is so important to have a structured performance management process that helps to control costs and justifies merit increases for those employees who perform well.

When organizations manage worker performance, they can control biases associated with managing employees and provide the framework for rewarding strong performers – while identifying poor performers.

A performance appraisal document is a key tool used in assessing performance.

When employees are scored on dimensions of performance, and those scores are tied to percentage increases, good performers get rewarded with a higher percentage of the pot.

Scoring the performance appraisal form and then tying the scores to raise distribution is an objective way to ensure your best performers are receiving a higher percentage of allocated raise dollars.

Ok, let’s look at the performance appraisal document again and see the dimension scores and look at this example:

Let’s say there are 7 dimensions that are being scored and for dimension one the employee received a score of 3, dimension two a score of 3, dimension three a score of 4, and so on.

Dimension one Score = 3

Dimension two Score = 3

Dimension three Score = 4

Dimension four Score = 3

Dimension five Score = 5

Dimension six Score = 3

Dimension seven Score = 4

Total score = 25

What you want to do is total the scores.

In this particular example if you add up the dimension scores you get a total score of 25 out of a possible 35 (7 dimensions X 5 points).

Now if you take that score of 25 and divide it by 7 (the number of dimensions), you get an average score of 3.5 – (25/7 = 3.5).

This is the score that will determine the employee’s percentage merit increase.

Next, you want to do this on all of your employees and come up with a list of average scores.

Ok, we’ve got the scores, but how do you tie those scores to raises?

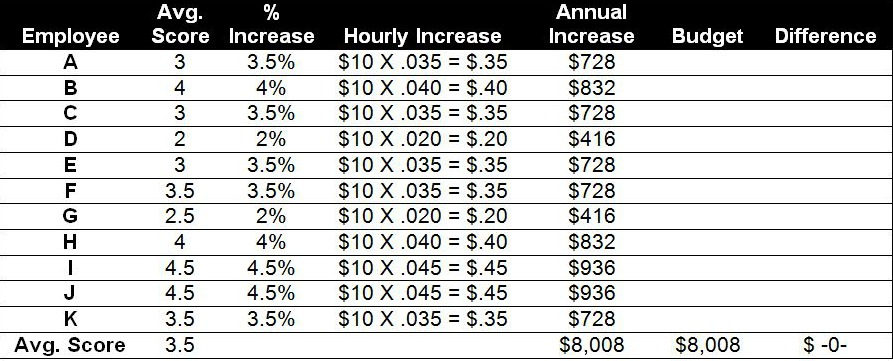

Let’s go through an example. Let’s say (for the sake of easy math) that you have:

- 11 employees each making $10/hour

- you budgeted 3.5% for raises which generates a pool of merit increase dollars of $8,008 (.035X$228,800). The $228,800 comes from 11 employees X 2080 hours X $10/hour = a salary budget of $228,800.

Now let’s also say that you have determined that the average performance appraisal scores (3.0) will receive a 3.5% increase – and those scoring below average will receive less, those scoring above will receive more.

Now let’s look at what this might look like:

As you can see from the example below, there are 11 employees listed, a,b,c, etc.

The next column shows their average scores as well as an overall average score for all employees.

Now, in the next column, you can see the percent increase that was awarded to each employee based on the predetermined criteria.

Some employees received as low as 2% increase, and the higher performers received as high as 4.5% increase which translates into a raise of $416 for the poor performers but more than twice as much, $936 for the higher performing employees.

Now if you total what all of these increases add up to, you’ll see that these pay increases will cost the organization $8,008 which ends up being exactly what was budgeted – $8008.

This is an oversimplified example to demonstrate how this can be done. Obviously, when there are dozens or even hundreds of employees, this scenario would look much different.

It is common for larger organizations to allocate the raise percentages to the individual department and allow managers to award raises specifically to their own area.

Another thing to remember is the importance of organizational culture and communicating clearly with all employees about their raise increases.

The higher performers should be aware that they received a higher percentage, but the lower performers should also be told that they received less because of their performance scores.

This should serve as an encouragement for the good performers and possibly a wake-up call for the underperformers.

And lastly, it doesn’t matter how high the raise percentage is. Most employees don’t think it’s enough, and that is just something you need to be aware of and not get overly concerned with.

It should not be a surprise but most people don’t think they are paid for what they believe they are worth and that organizations have unlimited resources for salaries – we know that’s not true.

Create a system to manage how employees are monitored and rewarded for what they do so you can be objective and deliberate in how merit increases are distributed!